How Much Home Can I Buy in Fresno in 2026?

Market Status: April 2026 Fresno Update

The 2026 Fresno Buying Strategy in 60 Seconds

The median Fresno home price is currently anchoring near $430,000. However, due to fluctuating builder incentives and the Central Valley "Heat Tax" (PG&E rates hitting 41.46¢/kWh), your monthly payment is a much more accurate indicator of affordability than the sticker price. The winning strategy in 2026 requires balancing the "Trinity" of Real Estate: Purchase Price, Interest Rate, and Monthly Payment.

How Much Home Can You Buy in Fresno in 2026?

At All Elite Homes, brokered by Epique Realty, we see the exact same mistake every week: buyers beginning their search by scrolling through Zillow and fixating on a "dream price" they got from a generic online calculator. In the Fresno market, that approach is not just flawed—it is financially dangerous.

Buying a home in the Central Valley requires a far more sophisticated lens. You are not just buying a structure; you are buying a monthly lifestyle cost. Before you speak to a lender, and long before you step inside an open house, you need to understand the underlying mechanics of what your money actually buys in our specific geography.

They say a "jack of all trades is a master of none," but most people forget the rest of the quote: "...but oftentimes better than a master of one." In the Fresno real estate market, being a master of the full system—from builder financing math to utility costs to school district boundaries—is the only way to truly protect a buyer. Here is the full playbook.

1. The Pre-Strategy Phase: Why the Lender Isn't Step One

The traditional advice is to "talk to a lender first." We disagree. Your first step should be a Strategy Call. A lender will tell you what you are technically approved to borrow based on gross income. But a lender does not know that your family loves taking weekend trips to Cambria, or that you have a $600 monthly daycare bill, or that you want to maintain your current lifestyle.

If you qualify for a $3,500 monthly mortgage, that doesn't mean you should take it. We help you find the "Comfort Number." Once we know the payment you can safely carry while still enjoying your life, then we connect you with a trusted lender to verify the financing. We build the strategy; the lender builds the loan.

2. The Trinity: Price, Rate, and Payment

To win in 2026, you must understand the Trinity of Home Buying. All three factors matter, but they do not matter equally.

- Purchase Price: The sticker price. It is often negotiable, but it is just a starting point.

- Interest Rate: The cost of the money. Rates can be temporarily bought down, permanently bought down, or refinanced in the future.

- Monthly Payment: The undeniable truth. This is the number that either gives you peace of mind or makes you "house poor."

Price is a distraction. You can negotiate a $500,000 home down to $480,000, but if the interest rate attached to that mortgage is a point higher, your monthly cost could actually be more than the original price. Conversely, a $525,000 new construction home might feel like a stretch, but with a builder-paid rate buydown, it could cost you $400 less per month than a cheaper resale home.

Pro Tip:

Falling in love with a home before your strategy is set leads to emotional whiplash. Read our guide on why Fresno buyers must get pre-approved before touring homes.

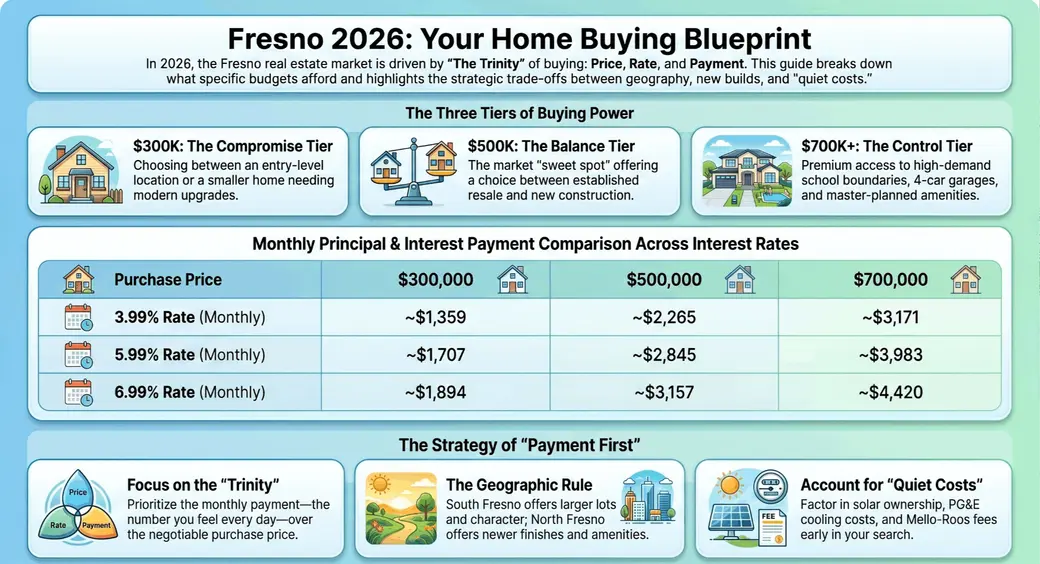

3. The Fresno Price Tiers: What Your Money Actually Buys

To give you a baseline for the greater Fresno area, we look at three major anchor points. Keep in mind, these are not hard ceilings—they are the bands where different lifestyle choices become available.

The $300,000 Tier: The Entry & Compromise

In 2026, $300,000 represents the entry point for the Fresno market. At this tier, you are typically choosing Location over Condition or Square Footage over Modernity. You may find an older, charming bungalow in the Tower District that boasts incredible character but features a 30-year-old roof. Alternatively, you might find a smaller condo in North Fresno that trades private yard space for a lower-maintenance lifestyle.

Many buyers at this tier love the Tower District because they prioritize culture, walkability, local coffee shops, and nightlife over school district rankings. It is a fantastic place to build equity, provided you budget for deferred maintenance.

The $500,000 Tier: The Balance Point

This is the sweet spot where the market truly opens up. At $500K, you are looking at well-maintained, established resale homes in desirable areas like The Bluffs or Old Town Clovis. This is also the primary battleground for new construction in the SEDA (Southeast Development Area) or Loma Vista corridors.

Buyers at this tier have the ultimate flexibility. You can choose the mature, tree-lined streets of an established neighborhood, or you can opt for the energy-efficient, warranty-backed peace of mind that comes with a brand-new build. This is also the price point where Clovis Unified School District (CUSD) homes become highly prevalent.

The $700,000 Tier: The Control Tier

At $700K and above, you are buying Control. You control the school district, the lot size, the square footage, and the finishes. This tier grants access to premium pockets like Copper River—a community known not just for luxury homes, but for a lifestyle built around fitness, golf, and highly-rated schools.

Homes at this tier often feature 3,000+ square feet, multi-car garages, high-end outdoor living spaces, and zero weekend renovation projects. You are buying a move-in-ready lifestyle.

Estimated 2026 Payment Examples by Price and Rate

To visualize the "Trinity," look at how the same purchase price feels entirely different based on the interest rate. (Note: We've used sample rates from 3.99% to 6.99% to illustrate the math of builder buydowns vs standard market rates).

| Price / Down | 3.99% | 4.99% | 5.99% | 6.99% |

|---|---|---|---|---|

| $300,000 (5% down) | ~$1,359 | ~$1,528 | ~$1,707 | ~$1,894 |

| $300,000 (20% down) | ~$1,144 | ~$1,287 | ~$1,437 | ~$1,595 |

| $500,000 (5% down) | ~$2,265 | ~$2,547 | ~$2,845 | ~$3,157 |

| $500,000 (20% down) | ~$1,907 | ~$2,145 | ~$2,396 | ~$2,659 |

| $700,000 (5% down) | ~$3,171 | ~$3,566 | ~$3,983 | ~$4,420 |

| $700,000 (20% down) | ~$2,670 | ~$3,003 | ~$3,354 | ~$3,722 |

*Estimates reflect Principal & Interest only on a 30-year fixed loan. They do not include property taxes, homeowners insurance, PMI, HOA dues, or solar obligations. Some buyers may qualify for 3.5% down FHA loans, which alters the total payment. All Elite Homes is not a lender.

4. The Geographic "Lot Size Inverse" Rule

In the Fresno area, there is a unique geographic phenomenon we teach all our buyers: As purchase price goes up, lot size often goes down.

Older central and southern neighborhoods (like Fig Garden) were built decades ago when land was cheap. You may easily find a $450K home sitting on a massive 12,000 square-foot lot with towering, mature shade trees—which is incredibly valuable for keeping summer AC costs low.

Conversely, a $650K brand-new home in a master-planned community might only offer a 5,500 square-foot lot. You are trading land size for modern finishes, district demand, and neighborhood amenities. Neither is objectively "better"—it simply depends on whether your family values hosting backyard barbecues or having a maintenance-free weekend.

5. Cross-Shopping the 45-Minute Spread (And The Commute Math)

One of the biggest mistakes a Fresno-area buyer can make is drawing a tiny circle on a map and refusing to look outside it. The reality of the Central Valley is the 45-Minute Spread.

Buyers routinely cross-shop Fresno, Clovis, Madera, Sanger, Riverstone, and Tesoro Viejo. A 30-to-45-minute drive can connect you to entirely different affordability brackets. However, we also make our clients do the "Commute Math." If you move to a beautiful new build in Madera but commute daily to South Fresno, you must factor in the cost of gas, vehicle wear-and-tear, and your personal time. Sometimes, paying slightly more for a central home is actually cheaper monthly than paying less for a home with a grueling commute.

6. New Build vs. Resale: A Masterclass in Strategy

At All Elite Homes, we love new construction. But we don't love it because of the fresh paint; we love it because of the financial leverage. Builders like Lennar, Granville, McCaffrey, De Young, Wilson Homes, and KB Home possess internal financing arms that allow them to offer incentives standard sellers cannot.

The Buydown Breakdown: You will often see builders offering rate buydowns.

A 2-1 Buydown is a temporary band-aid: your rate is 2% lower the first year, 1% lower the second year, and then returns to the standard market rate.

A Permanent Buydown means the builder pays massive cash at closing to lower your rate for the entire 30-year life of the loan. This is where a $550,000 new build can miraculously have a lower payment than a $490,000 resale home.

Case Study: The $325K Pivot

"We recently represented a buyer qualified for a $325,000 purchase. The resale homes in their initial target area technically fit the budget, but they needed major work and didn't fit the family's long-term goals. Instead of settling, we pivoted. We looked at a new construction community slightly farther out that they hadn't even considered. By leveraging builder closing cost credits, we bought their interest rate down significantly. The result? They moved into a brand-new, energy-efficient home, with a better school-district fit, for a payment they could comfortably afford. That is strategy."

7. The "Quiet Costs" of 2026: PG&E and The Heat Tax

In Fresno, the list price is never the whole story. If you aren't calculating the "Quiet Costs," you are flying blind.

The most brutal of these is the Heat Tax. As of 2026, PG&E rates sit around 41.46¢ per kWh, alongside a new $24 monthly Base Services Charge. A home with poor insulation and a 20-year-old AC unit will punish your wallet from June through September. Furthermore, you must look at solar carefully: Owned Solar adds massive equity and lowers your bill cleanly. A Solar Lease or PPA (Power Purchase Agreement) acts as a lien on the house, affects your Debt-to-Income ratio, and can create friction if you ever decide to sell.

You also need to account for HOA dues (which directly reduce your buying power) and Mello-Roos/CFDs (special tax assessments common in newer growth areas like Loma Vista).

For a deep dive into these numbers, read our comprehensive guide: How much it costs to run a home in Fresno.

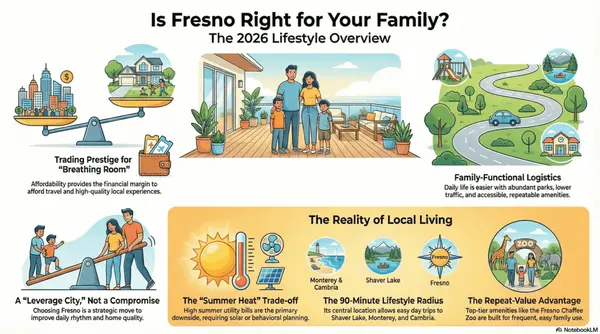

Is Fresno Right For Your Family?

Between the school districts, the parks, and the lifestyle amenities, the Central Valley has a lot to offer. Find out if it's the right fit for your long-term goals.

Read the Fresno Family Guide8. Fresno Home Buying FAQ

Is it the right time to buy a house in Fresno?

Yes, if you can afford the payment and the home fits your life. Buying now allows you to enter the market and start building equity. If rates drop later, you can potentially refinance. Waiting for "perfect conditions" often backfires because when rates drop, buyer competition floods the market and prices rise. Ask friends who bought in 2010 or 2015—they rarely regret their timing.

Will interest rates go down this year?

Nobody knows for sure. What we do know is that some markets create unique opportunities through builder incentives, seller credits, and rate buydowns. The better question is not "will rates go down," but rather "what payment can I safely afford today?"

Can I buy in Clovis Unified while living in Fresno?

Yes. A Fresno address does not automatically mean Fresno Unified. Many Fresno addresses (especially in North and Northeast Fresno) are inside Clovis Unified School District boundaries. Buyers should always verify the school boundary map, not just the city name.

Is Fresno Unified always a bad option?

No. While Clovis Unified carries strong market demand, Fresno Unified offers standout specialty schools and magnet programs, such as University High School and Design Science Middle College High. District reputation matters, but buyers should look at the specific school, the commute, the neighborhood, and their own family priorities before writing off an entire district.

How much income do I need to buy a home in Fresno?

There is no single income number because lenders qualify buyers based on a complex web of factors: debt-to-income ratio, down payment, credit profile, taxes, insurance, and HOA dues. The practical answer is to start by determining the monthly payment you are comfortable with, and then let a professional verify what purchase price that payment supports.

Are builder incentives better than seller credits?

Sometimes. Builder incentives can be incredibly powerful because they are often large enough to permanently buy down the interest rate, significantly reducing your monthly payment. While resale sellers can offer credits, they rarely have the profit margins to compete with a corporate builder's financing incentives.

Can HOA dues or solar leases change how much home I can buy?

Yes. HOA dues and solar lease/PPA payments count against your total monthly debt-to-income ratio. A condo that looks $50,000 cheaper on paper might actually cost you more monthly if it carries a $400/month HOA fee. Likewise, a solar lease must be factored into your qualification limits.

Are All Elite Homes agents lenders?

No. All Elite Homes is a real estate team, not a lender. Our job is to help you compare Fresno-area neighborhoods, new build options, resale homes, and payment strategies. Once the strategy is built, we connect you with a licensed mortgage professional to execute and verify the financing details.

Next Step for Fresno Home Buyers

Do not guess your way into a purchase this big. Start with All Elite Homes as your first call. We will help you compare payment bands, new build incentives, resale tradeoffs, and the lifestyle fit behind the numbers. Then, we connect you with a lender to verify the financing.

Get a custom payment breakdown & compare new build vs. resale.

Categories

Recent Posts

GET MORE INFORMATION